The End of PDF Invoices in Germany

Why 2025–2028 Marks the Structural Shift from Documents to Data

For two decades, PDF invoices have been the default in German B2B.

They feel digital.

They arrive by email.

They are archived in folders.

But legally speaking, a PDF is no longer the future format of German business.

Between 2025 and 2028, Germany transitions from “PDF tolerated” to structured electronic invoice required.

This is not a software upgrade.

It is a regulatory infrastructure shift.

The Legal Backbone: What Changed

Germany amended §14 UStG under the Growth Opportunities Act (Wachstumschancengesetz).

The key change:

An electronic invoice is now legally defined as:

A structured electronic format that enables automated processing.

A PDF does not meet this definition.

It is classified as a “sonstige Rechnung” — an “other invoice.”

That category is transitional.

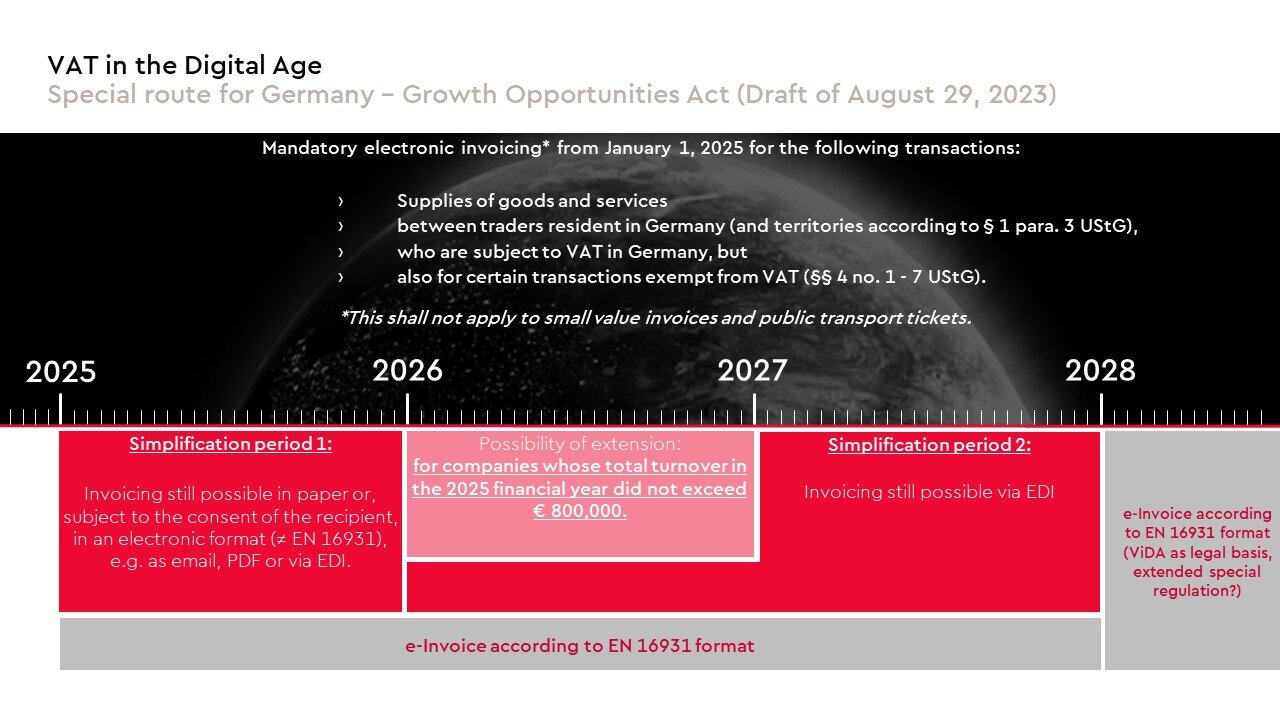

The Timeline: 2025 → 2028

1 January 2025

All German businesses must be able to receive structured electronic invoices for domestic B2B.

Even if you continue sending PDFs, you must technically accept EN 16931-compliant invoices.

1 January 2027

Businesses with prior-year turnover above €800,000 must issue structured invoices.

For these companies, PDF effectively stops being compliant for domestic B2B.

1 January 2028

All domestic B2B invoices must be structured electronic invoices.

PDF invoices between taxable persons are no longer legally sufficient in most cases.

Small-business exemptions exist for issuance, but the direction is clear:

Structured becomes the default.

PDF becomes legacy.

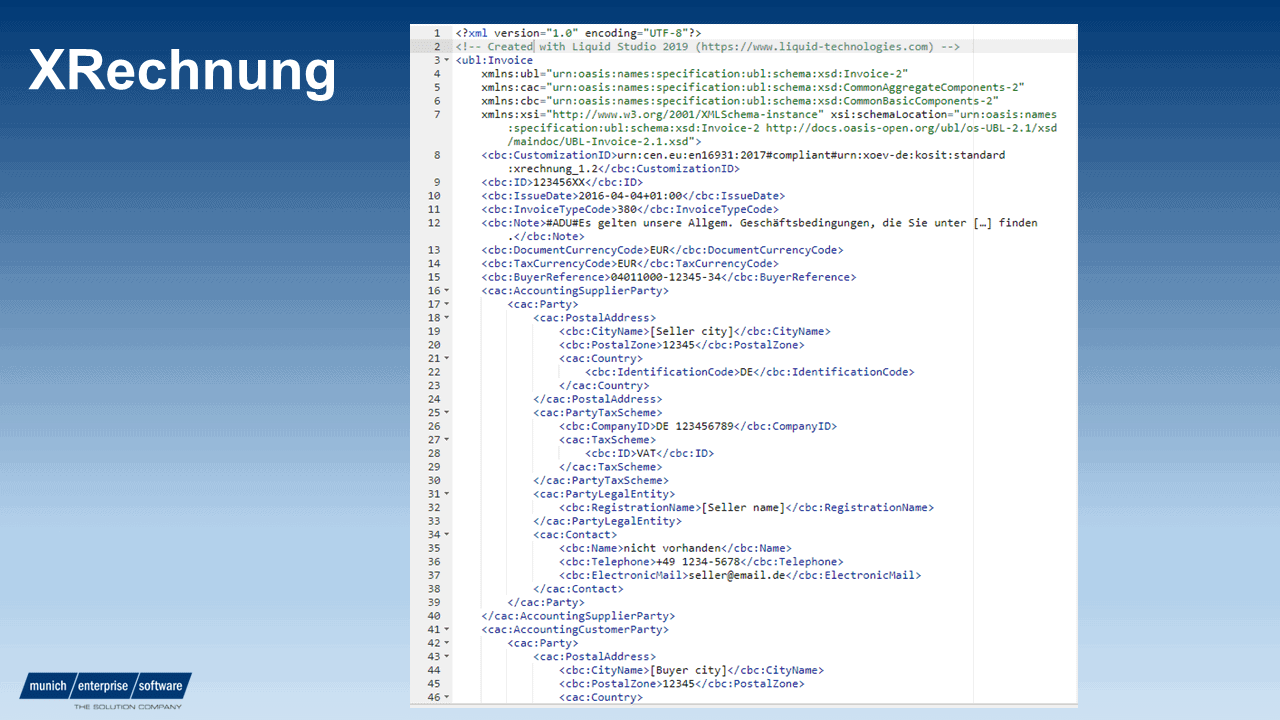

What “Structured” Actually Means

Germany references the European standard EN 16931.

Common compliant formats:

- XRechnung

- ZUGFeRD (from version 2.0.1 onward)

These formats contain machine-readable XML data.

A PDF is visual.

An EN 16931 invoice is data-first.

This distinction matters because the law no longer cares about readability for humans.

It cares about extractability for systems.

Why This Is Not Just a Format Change

Many founders interpret this as:

“We’ll just switch invoice export format in our accounting tool.”

That misses the structural shift.

The new system assumes:

- Automated processing

- System-to-system compatibility

- Future digital reporting integration

This aligns directly with the EU’s VAT in the Digital Age (ViDA) initiative, which introduces cross-border digital reporting by 2030.

Germany’s domestic mandate is not isolated.

It is preparatory infrastructure.

The Risk Side: What If You Ignore It?

Once transitional periods expire:

- Failure to issue proper invoices can trigger administrative fines.

- Input VAT deduction may be denied if the invoice format does not meet §14 requirements.

- Audit exposure increases as structured data becomes standard.

The financial impact is not hypothetical.

If an invoice is formally invalid, VAT deductibility is at risk.

That is a structural accounting risk, not a formatting issue.

The Hidden Shift: From Documents to Tax Infrastructure

The deeper change is conceptual.

Invoices are no longer documents.

They are data packets.

When Germany mandates structured B2B invoices, it effectively moves invoice exchange into regulatory infrastructure.

That has consequences:

- Archive systems must handle structured data.

- Intake systems must preserve machine-readable content.

- Storage systems must remain audit-proof.

- Multi-entity structures must segregate invoice flows correctly.

A shared Google Drive folder with PDFs is not designed for this.

What This Means for SMEs

If you are running:

- One GmbH

- Multiple operating entities

- Cross-border structures (Germany + Austria, Germany + Slovenia)

Your document workflow is no longer neutral.

Between 2025 and 2028, it becomes compliance-sensitive.

The question is not:

“Can we store PDFs?”

The question is:

“Is our intake and archive system aligned with structured invoice law?”

A Structural Reframing

For 15 years, document management was an efficiency problem.

Now it is a regulatory alignment problem.

The companies that adapt early will experience:

- Cleaner accounting flows

- Lower reconciliation overhead

- Lower audit friction

- Better cross-border readiness

The companies that ignore it will adapt reactively under pressure.

The Real Ending

PDF invoices are not disappearing tomorrow.

But they are transitioning from default to exception.

Germany has made that direction explicit.

The period 2025–2028 is not a technical migration window.

It is the end of the PDF era as a legally sufficient B2B standard.

And once structured invoices become mandatory, the intake system stops being an admin tool.

It becomes part of your compliance architecture.